Retirement is a period of life where one has to be financially secure. However, this is a period that needs some strategic planning. One of the best methods employed in ensuring that consistent income is maintained during retirement is by use of a system withdrawal plan. In this plan, you set a specific amount to withdraw from your investment account after a short period, whereby this money works as a fixed income. An SWP calculator should be viewed as a significant process in ensuring that the optimization process is achieved. Let’s discuss factors necessary when utilizing this tool for effective planning on retirement income.

What Is An SWP Calculator?

An SWP calculator is an online application that explains to a mutual fund investor the benefits of systematic income withdrawal from their investments without exhausting the funds too soon. With the calculator various models are run, varying the lump sum investment, withdrawal percentages, investment returns and the time period within which withdrawals are made. Such a technique is useful in assessing how long either of your investments will last and if your level of expectations concerning income is plain realistic.

Guidelines For Using An SWP Calculator

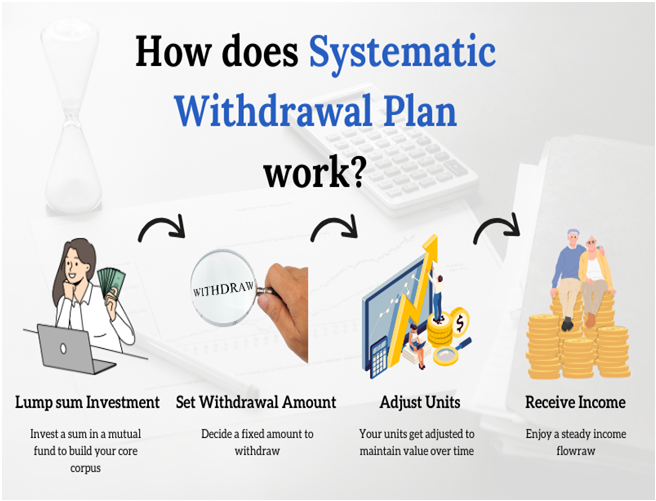

- Welcome or Greet Enter The Amount You Would Like To Invest The very first step is to input the overall amount of money you have made a lump sum investment in either equity mutual funds or any other asset type. This acts as a starting point for your scheduled withdrawals.

- Select the Amount or Rate for Your Withdrawals Bring what you need to the table next. Monthly or annual withdrawals (ideally, only a portion of the accumulated value). The calculator will help in determining the length of time this amount will last against the monthly withdrawals made in the given month with a given withdrawal rate.

- Enter the Expected Rate of Return In most cases the expected withdrawal strategies also incorporate an expected rate of return on investment. This is important because most of the time; the amount withdrawn must not be more than the amount earned. Although you can apply a higher estimation, it is safer to be conservative to avoid running short of funds.

- Determine the Withdrawal Duration This is the time over which you wish to make withdrawals. If for instance, you are anticipating income from your investments for the next 20 years, the calculator will indicate if the withdrawals will consume the investment corpus before that duration.

- Check the Outputs All these details enriched will also bring the calculator to show up clear details regarding the time elapsed before the expected amounts are withdrawn. It indicates the period within which the corpus would last if there are no other inflows and whether it would be possible to achieve the desired inflow each month. If this is not the case, the withdrawal sum may have to be changed or the initial invested amount re-considered.

An SWP Calculator Has Some of The Following Benefits

- Proper Budgeting: Thanks to an SWP calculator, you understand how much you can get during your retirement and you will be able to plan properly.

- Saves you from Overdrawing You: It saves you from withdrawing more at once or early on which answers the problem of having money finishes fast.

- Scenario Testing: You can test multiple scenarios, scenarios like changing the withdrawal rate, changing the investment period or changing the expected return to see which one best suits your requirements.

Making the Most Out of Your SWP in Retirement

In as much as SWP/SWP calculators are used in planning, there are several main strategies that should be kept in mind.

- Have a Low Initial Withdrawal Ratio: Most experts agree that it is safe to begin taking out roughly 4 to 5 percent of your portfolio every year. This is to make sure that the remaining funds would still be intact in case of market highs or lows.

- Review Regularly: Time might bring changes in the market as well as in the person’s underlying requirement. Regularly review your baseline-and current-withdrawal plan and update it to reflect your needs and current market factors.

- Use with Other Sources of Income: SWP usage in retirement should be used with pension funds or property rental income or savings.

Summary

After determining how much you intend to save for retirement, planning for it becomes easier, though it may seem hard. But an SWP calculator helps you ensure that you have an acceptable level of risk when coming up with a driven or distribution plan. By inputting your investment, withdrawal amount, and expected rate of return, you can easily see how long your savings will last. With careful planning and periodic adjustments, an SWP can be a reliable source of income, ensuring financial peace of mind throughout your retirement.